When your roof gets damaged and you file a claim, the insurance adjuster's first estimate often comes in lower than what local roofers actually charge to do the work right. You end up in a gap between what the insurance company wants to pay and what the repair actually costs. This happens regularly in Texas, and it's not because adjusters are dishonest. They work from templates and don't always account for local labor rates, material availability, or the specific condition of your roof. You have leverage in this negotiation, and knowing how to use it makes a real difference in what you'll pay out of pocket.

Get a detailed written estimate from a local roofer first

Before you push back on anything, hire a roofing contractor to inspect the damage and provide a written estimate. This isn't about getting a second opinion. It's about having a document that speaks the insurance company's language. The adjuster's estimate is one number. A licensed local roofer's estimate is a professional assessment based on what the work actually costs here, in your area, with real material prices and real labor rates. When you submit this estimate, you're not arguing. You're presenting evidence. Make sure the estimate includes a breakdown of materials, labor, and any necessary repairs to the underlying structure. Spartan Roof Construction can provide this kind of detailed estimate for you.

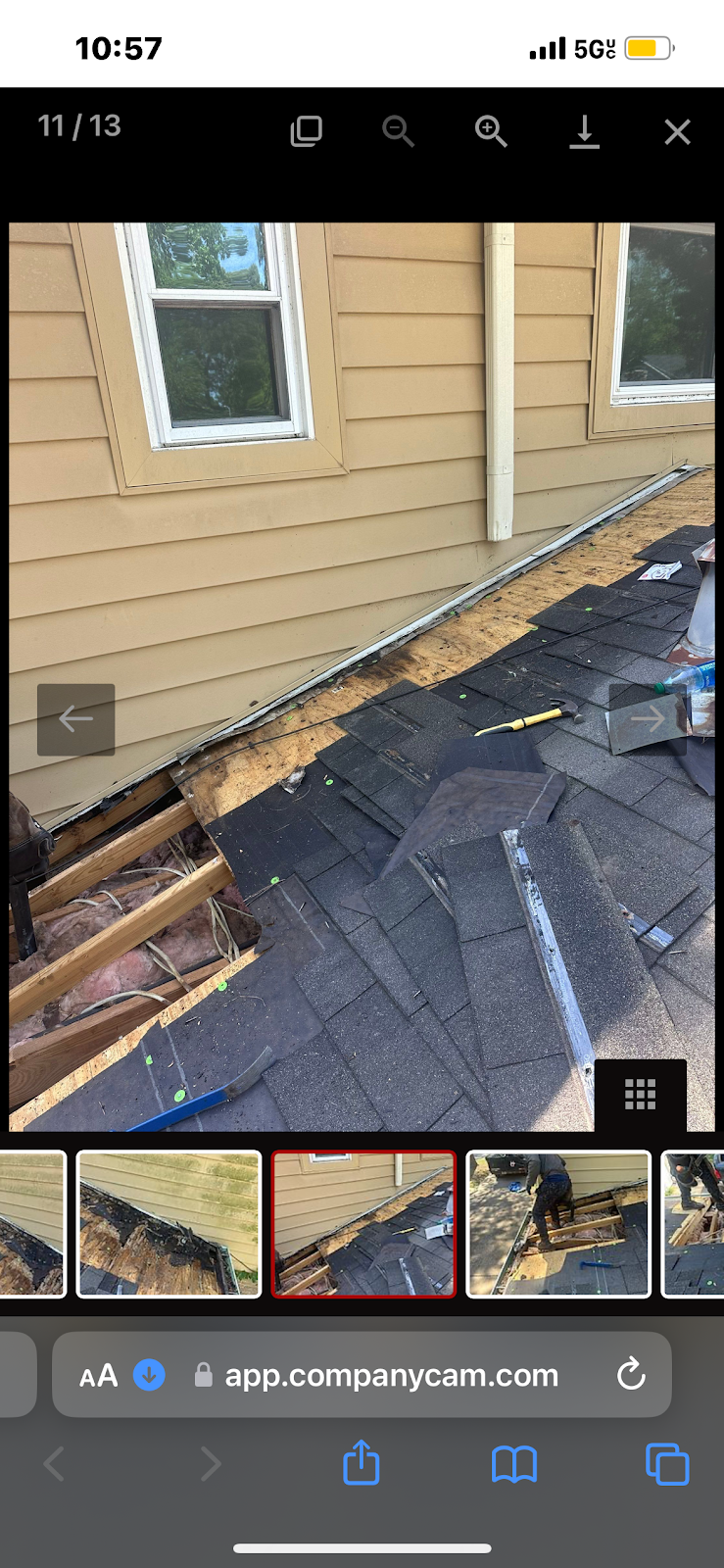

Document everything the adjuster may have missed

Walk the roof yourself after the initial inspection, or have your roofer do it with you. Take photos and video. Insurance adjusters sometimes miss secondary damage, especially if they're moving fast through multiple claims after a storm. They might not account for damaged flashing, worn decking under the shingles, or deterioration that's been there longer than the recent damage. If your roof is older, the adjuster might use depreciation tables that don't reflect what replacement actually costs. When you have your roofer's estimate, it will include these details. Use them. If the adjuster missed something, point it out with specifics: "Your estimate doesn't include the east-facing flashing, which shows separation in photos taken on [date]." This isn't confrontational. It's factual.

Request a formal appraisal if the numbers don't match

Most insurance policies include an appraisal clause. If you and the insurance company disagree on the cost to repair, either party can request an appraisal. This means an independent, neutral third party reviews both estimates and makes a binding decision. The process costs money, but it's often worth it if the gap is significant. You'll need to hire an appraiser, the insurance company will hire one, and if those two disagree, a third appraiser is selected. The cost is usually split. An appraisal forces the insurance company to take the disagreement seriously. Many adjusters will reconsider their estimate rather than go to appraisal, because it's expensive for them too and because an independent professional often sides with the contractor's estimate.

Understand what depreciation really means

Depreciation is where a lot of disputes happen. The insurance company deducts an amount for wear and tear, especially on older roofs. But depreciation doesn't mean your roof is worthless. It means the insurance company is trying to avoid paying for a full replacement when they're only fixing storm damage. If your roof was damaged by hail or wind, and the damage is localized, the adjuster might deduct depreciation from the entire roof even though you're only repairing part of it. That's worth pushing back on. Ask the adjuster to justify the depreciation percentage and show you the breakdown. If your roof is only five or six years old, heavy depreciation doesn't make sense. If it's older but well-maintained, you can argue that. Your roofer's estimate should address this directly.

Work with your roofer as your advocate

This is important. Your roofer isn't just providing an estimate. They can help you navigate the insurance process. Roofers deal with insurance companies constantly and know what adjusters typically accept and what they push back on. Some roofers will attend the adjuster's inspection with you, or request to be there. Having the contractor present keeps the conversation factual and prevents the adjuster from making claims about the work that the roofer can immediately correct. Your roofer can also write a follow-up letter to the insurance company if the estimate comes in low, detailing why their original estimate is accurate. This carries weight because it's from a licensed professional with liability on the line.

Know when to walk away from negotiation

Not every dispute is worth pursuing. If the gap between estimates is a few hundred dollars on a large job, it might be easier to cover it yourself than to spend time and money on an appraisal. But if the gap is substantial, if the damage is extensive, or if the adjuster clearly missed something, negotiation or appraisal makes sense. Don't let frustration push you into a decision. Get clear numbers, understand what's being disputed, and decide based on the actual cost difference.

The insurance process moves slowly by design. Stay patient, stay organized, and keep everything in writing. When you're ready to move forward with repairs, Spartan Roof Construction can help you understand your options and get the work done right. Call us to discuss your estimate and next steps.